Momentum Trader Strategy 3.0Momentum Trader 3.0 is a momentum trading strategy which uses volume to confirm market momentum driven moves.

By default it only trades between 0900 and 1530 (designed for futures trading and can be toggled to 24/7)

No repaint issues, what you see is real

Toggles allow you to enable Long or Short independently which may work better or worse for your market

Designed primarily for Day Trading (1-15m interval)

Presently only the Short side is optimized, the Long works but overtrades a bit. I will be adding an option to remove the less useful signals and improve performance.

Momentum Trader is a real and successful momentum strategy (which I use myself). It isn't a miracle 'always win' strategy but it is a steady workhorse. By combining high probability momentum trades and auto stop-losses, it takes a good slice of most rallies, a big slice of the grand drops, and avoids heavy sudden losses.

Momentum Trader can be used in any timeframe. Your success depends on the volatility of the individual market. I recommend trading at 10m and below for high volatility instruments like ES/SPX while low volatility instruments can be traded at the 1h and beyond. At the level of 1D+ it also works as well but naturally as a momentum strategy it may take a while to pivot.

Momentum Trader provides you with 3 long and 2 short entries which represent different levels of risk/reward. Like any real strategy, there can be periods of chop where the strategy will lose (small based on stop-loss) if the market is chopping very quickly back and forth or pivoting suddenly. As a rule, Momentum Trader attempts to avoid most of that by typically flagging trends which are established and confirmed. Different signals give you different degrees of confirmation and thus different risk/reward.

Cerca negli script per "stop loss"

Default Strategy Inputs (Forex / Crypto)The code in this post contains a set of default strategy inputs I use in new projects / backtests in Tradingview.

Full code commentary is available on the Backtest-Rookies website. To comply with house rules, I cannot post the direct link here.

Features

Trade Direction: So that you can limit the strategy for long only, short only or trade in both directions. It is important to note that when you select “Long Only”, you will still see Short signals on the chart. However, they are only used to close a position rather than reverse it. This is the default behaviour for strategies. The same applies to “Short Only”.

Date Ranges: So that you can isolate backtesting to specific periods of interest such as bull or bear markets.

Sessions: So you can easily get an idea of the expected results during your own session. You may also notice that performance of the strategy varies depending on which session it is deployed in.

Some example stop losses: It is not an exhaustive list but it should be enough to provide some inspiration for different types of stops that you can experiment with.

Happy Scripting. I hope the community finds it useful.

Macro-Filtered Volatility Breakout (MVB)策略簡介:

這是一套專門針對高 Beta 值資產(如 ETH, SOL 等山寨幣)設計的趨勢跟隨系統。我們解決了傳統突破策略在山寨幣市場中「假突破(False Breakout)」過多的痛點。

核心邏輯:

市場體制過濾(Regime Filtering): 加密貨幣市場具有高度的相關性。本策略引入比特幣(BTC)作為**「宏觀市場指標」**,只有當 BTC 處於確立的多頭趨勢時,才允許執行山寨幣的做多信號。這有效規避了「大盤崩盤時,小幣假突破」的系統性風險。

動態波動率通道: 我們不使用固定價格止損,而是採用肯特納通道(Keltner Channels)。這利用 ATR(平均真實波幅)動態調整進出場區間:在市場平靜時通道收窄以敏銳捕捉啟動點,在劇烈波動時通道放寬以避免被雜訊洗出場。

風控特徵:

系統性避險: 透過 BTC 趨勢濾網,在熊市或大盤回調期間自動空手,降低回撤。

獲利奔跑(Let Profits Run): 採用基於波動率的移動止損(Volatility Trailing Stop),在大趨勢中能吃到完整的魚身。

免責聲明:

以上策略分享僅供學術研究、回測實驗與邏輯參考,並不代表對未來獲利的保證。 過往的回測績效不代表未來的行情表現。本文內容不構成任何投資建議。加密貨幣交易具有高度風險,使用者應自行評估風險承受能力並自負盈虧,本人不承擔任何因使用此策略而產生的資金損失。

Strategy Overview

This is a trend-following system specifically designed for high-beta assets, such as altcoins like ETH, SOL, and similar cryptocurrencies. The strategy addresses a key weakness of traditional breakout systems in altcoin markets—the high frequency of false breakouts.

Core Logic

Market Regime Filtering

The cryptocurrency market exhibits strong cross-asset correlation. This strategy uses Bitcoin (BTC) as a macro market indicator. Long signals on altcoins are only allowed when BTC is in a confirmed bullish trend, effectively avoiding the systemic risk of altcoin false breakouts during broader market downturns.

Dynamic Volatility Channels

Instead of fixed-price stop losses, the strategy employs Keltner Channels, which adapt dynamically using ATR (Average True Range).

During low-volatility conditions, the channel narrows to sensitively capture early trend initiation.

During high-volatility environments, the channel widens to prevent premature exits caused by market noise.

Risk Management Features

Systematic Risk Avoidance

By applying BTC trend filtering, the strategy automatically stays in cash during bear markets or major market pullbacks, significantly reducing drawdowns.

Let Profits Run

A volatility-based trailing stop is used to maximize profit capture during strong directional trends, allowing positions to benefit from the full trend structure.

Disclaimer

The strategy presented above is for academic research, backtesting experiments, and logical reference only. It does not constitute a guarantee of future performance. Past backtest results are not indicative of future outcomes. This content does not represent any investment advice. Cryptocurrency trading involves substantial risk, and users should assess their own risk tolerance and assume full responsibility for any gains or losses. The author bears no liability for any financial losses incurred from the use of this strategy.

SP500 Session Gap Fade StrategySummary in one paragraph

SPX Session Gap Fade is an intraday gap fade strategy for index futures, designed around regular cash sessions on five minute charts. It helps you participate only when there is a full overnight or pre session gap and a valid intraday session window, instead of trading every open. The original part is the gap distance engine which anchors both stop and optional target to the previous session reference close at a configurable flat time, so every trade’s risk scales with the actual gap size rather than a fixed tick stop.

Scope and intent

• Markets. Primarily index futures such as ES, NQ, YM, and liquid index CFDs that exhibit overnight gaps and regular cash hours.

• Timeframes. Intraday timeframes from one minute to fifteen minutes. Default usage is five minute bars.

• Default demo used in the publication. Symbol CME:ES1! on a five minute chart.

• Purpose. Provide a simple, transparent way to trade opening gaps with a session anchored risk model and forced flat exit so you are not holding into the last part of the session.

• Limits. This is a strategy. Orders are simulated on standard candles only.

Originality and usefulness

• Unique concept or fusion. The core novelty is the combination of a strict “full gap” entry condition with a session anchored reference close and a gap distance based TP and SL engine. The stop and optional target are symmetric multiples of the actual gap distance from the previous session’s flat close, rather than fixed ticks.

• Failure mode it addresses. Fixed sized stops do not scale when gaps are unusually small or unusually large, which can either under risk or over risk the account. The session flat logic also reduces the chance of holding residual positions into late session liquidity and news.

• Testability. All key pieces are explicit in the Inputs: session window, minutes before session end, whether to use gap exits, whether TP or SL are active, and whether to allow candle based closes and forced flat. You can toggle each component and see how it changes entries and exits.

• Portable yardstick. The main unit is the absolute price gap between the entry bar open and the previous session reference close. tp_mult and sl_mult are multiples of that gap, which makes the risk model portable across contracts and volatility regimes.

Method overview in plain language

The strategy first defines a trading session using exchange time, for example 08:30 to 15:30 for ES day hours. It also defines a “flat” time a fixed number of minutes before session end. At the flat bar, any open position is closed and the bar’s close price is stored as the reference close for the next session. Inside the session, the strategy looks for a full gap bar relative to the prior bar: a gap down where today’s high is below yesterday’s low, or a gap up where today’s low is above yesterday’s high. A full gap down generates a long entry; a full gap up generates a short entry. If the gap risk engine is enabled and a valid reference close exists, the strategy measures the distance between the entry bar open and that reference close. It then sets a stop and optional target as configurable multiples of that gap distance and manages them with strategy.exit. Additional exits can be triggered by a candle color flip or by the forced flat time.

Base measures

• Range basis. The main unit is the absolute difference between the current entry bar open and the stored reference close from the previous session flat bar. That value is used as a “gap unit” and scaled by tp_mult and sl_mult to build the target and stop.

Components

• Component one: Gap Direction. Detects full gap up or full gap down by comparing the current high and low to the previous bar’s high and low. Gap down signals a long fade, gap up signals a short fade. There is no smoothing; it is a strict structural condition.

• Component two: Session Window. Only allows entries when the current time is within the configured session window. It also defines a flat time before the session end where positions are forced flat and the reference close is updated.

• Component three: Gap Distance Risk Engine. Computes the absolute distance between the entry open and the stored reference close. The stop and optional target are placed as entry ± gap_distance × multiplier so that risk scales with gap size.

• Optional component: Candle Exit. If enabled, a bullish bar closes short positions and a bearish bar closes long positions, which can shorten holding time when price reverses quickly inside the session.

• Session windows. Session logic uses the exchange time of the chart symbol. When changing symbols or venues, verify that the session time string still matches the new instrument’s cash hours.

Fusion rule

All gates are hard conditions rather than weighted scores. A trade can only open if the session window is active and the full gap condition is true. The gap distance engine only activates if a valid reference close exists and use_gap_risk is on. TP and SL are controlled by separate booleans so you can use SL only, TP only, or both. Long and short are symmetric by construction: long trades fade full gap downs, short trades fade full gap ups with mirrored TP and SL logic.

Signal rule

• Long entry. Inside the active session, when the current bar shows a full gap down relative to the previous bar (current high below prior low), the strategy opens a long position. If the gap risk engine is active, it places a gap based stop below the entry and an optional target above it.

• Short entry. Inside the active session, when the current bar shows a full gap up relative to the previous bar (current low above prior high), the strategy opens a short position. If the gap risk engine is active, it places a gap based stop above the entry and an optional target below it.

• Forced flat. At the configured flat time before session end, any open position is closed and the close price of that bar becomes the new reference close for the following session.

• Candle based exit. If enabled, a bearish bar closes longs, and a bullish bar closes shorts, regardless of where TP or SL sit, as long as a position is open.

What you will see on the chart

• Markers on entry bars. Standard strategy entry markers labeled “long” and “short” on the gap bars where trades open.

• Exit markers. Standard exit markers on bars where either the gap stop or target are hit, or where a candle exit or forced flat close occurs. Exit IDs “long_gap” and “short_gap” label gap based exits.

• Reference levels. Horizontal lines for the current long TP, long SL, short TP, and short SL while a position is open and the gap engine is enabled. They update when a new trade opens and disappear when flat.

• Session background. This version does not add background shading for the session; session logic runs internally based on time.

• No on chart table. All decisions are visible through orders and exit levels. Use the Strategy Tester for performance metrics.

Inputs with guidance

Session Settings

• Trading session (sess). Session window in exchange time. Typical value uses the regular cash session for each contract, for example “0830-1530” for ES. Adjust if your broker or symbol uses different hours.

• Minutes before session end to force exit (flat_before_min). Minutes before the session end where positions are forced flat and the reference close is stored. Typical range is 15 to 120. Raising it closes trades earlier in the day; lowering it allows trades later in the session.

Gap Risk

• Enable gap based TP/SL (use_gap_risk). Master switch for the gap distance exit engine. Turning it off keeps entries and forced flat logic but removes automatic TP and SL placement.

• Use TP limit from gap (use_gap_tp). Enables gap based profit targets. Typical values are true for structured exits or false if you want to manage exits manually and only keep a stop.

• Use SL stop from gap (use_gap_sl). Enables gap based stop losses. This should normally remain true so that each trade has a defined initial risk in ticks.

• TP multiplier of gap distance (tp_mult). Multiplier applied to the gap distance for the target. Typical range is 0.5 to 2.0. Raising it places the target further away and reduces hit frequency.

• SL multiplier of gap distance (sl_mult). Multiplier applied to the gap distance for the stop. Typical range is 0.5 to 2.0. Raising it widens the stop and increases risk per trade; lowering it tightens the stop and may increase the number of small losses.

Exit Controls

• Exit with candle logic (use_candle_exit). If true, closes shorts on bullish candles and longs on bearish candles. Useful when you want to react to intraday reversal bars even if TP or SL have not been reached.

• Force flat before session end (use_forced_flat). If true, guarantees you are flat by the configured flat time and updates the reference close. Turn this off only if you understand the impact on overnight risk.

Filters

There is no separate trend or volatility filter in this version. All trades depend on the presence of a full gap bar inside the session. If you need extra filtering such as ATR, volume, or higher timeframe bias, they should be added explicitly and documented in your own fork.

Usage recipes

Intraday conservative gap fade

• Timeframe. Five minute chart on ES regular session.

• Gap risk. use_gap_risk = true, use_gap_tp = true, use_gap_sl = true.

• Multipliers. tp_mult around 0.7 to 1.0 and sl_mult around 1.0.

• Exits. use_candle_exit = false, use_forced_flat = true. Focus on the structured TP and SL around the gap.

Intraday aggressive gap fade

• Timeframe. Five minute chart.

• Gap risk. use_gap_risk = true, use_gap_tp = false, use_gap_sl = true.

• Multipliers. sl_mult around 0.7 to 1.0.

• Exits. use_candle_exit = true, use_forced_flat = true. Entries fade full gaps, stops are tight, and candle color flips flatten trades early.

Higher timeframe gap tests

• Timeframe. Fifteen minute or sixty minute charts on instruments with regular gaps.

• Gap risk. Keep use_gap_risk = true. Consider slightly higher sl_mult if gaps are structurally wider on the higher timeframe.

• Note. Expect fewer trades and be careful with sample size; multi year data is recommended.

Properties visible in this publication

• On average our risk for each position over the last 200 trades is 0.4% with a max intraday loss of 1.5% of the total equity in this case of 100k $ with 1 contract ES. For other assets, recalculations and customizations has to be applied.

• Initial capital. 100 000.

• Base currency. USD.

• Default order size method. Fixed with size 1 contract.

• Pyramiding. 0.

• Commission. Flat 2 USD per order in the Strategy Tester Properties. (2$ buying + 2$selling)

• Slippage. One tick in the Strategy Tester Properties.

• Process orders on close. ON.

Realism and responsible publication

• No performance claims are made. Past results do not guarantee future outcomes.

• Costs use a realistic flat commission and one tick of slippage per trade for ES class futures.

• Default sizing with one contract on a 100 000 reference account targets modest per trade risk. In practice, extreme slippage or gap through events can exceed this, so treat the one and a half percent risk target as a design goal, not a guarantee.

• All orders are simulated on standard candles. Shapes can move while a bar is forming and settle on bar close.

Honest limitations and failure modes

• Economic releases, thin liquidity, and limit conditions can break the assumptions behind the simple gap model and lead to slippage or skipped fills.

• Symbols with very frequent or very large gaps may require adjusted multipliers or alternative risk handling, especially in high volatility regimes.

• Very quiet periods without clean gaps will produce few or no trades. This is expected behavior, not a bug.

• Session windows follow the exchange time of the chart. Always confirm that the configured session matches the symbol.

• When both the stop and target lie inside the same bar’s range, the TradingView engine decides which is hit first based on its internal intrabar assumptions. Without bar magnifier, tie handling is approximate.

Legal

Education and research only. This strategy is not investment advice. You remain responsible for all trading decisions. Always test on historical data and in simulation with realistic costs before considering any live use.

U.T.M.S v2🇷🇺 ОПИСАНИЕ (РУССКИЙ)

U.T.M.S v2 — Чистый EMA-кроссовер с фильтрами

Стратегия для 15м (в первую очередь) и 1ч таймфреймов.

Генерирует сигналы при пересечении EMA(8) и EMA(19) только при подтверждении тренда, объёма, волатильности и времени суток.

Каждая сделка закрывается по фиксированному Take Profit и Stop Loss.

✅ Минимум ложных входов

✅ Работает только в ликвидные часы

✅ Полная фильтрация шума и флэта

🔧 Настройки:

Fast EMA / Slow EMA — периоды скользящих (по умолчанию 8 / 19)

Take Profit % — уровень фиксации прибыли (рек. 2.5%)

Stop Loss % — уровень стоп-лосса (рек. 2.0%)

Фильтры (все включены по умолчанию):

Use 1H Trend Filter — вход разрешён только по направлению тренда на 1H (EMA50 > EMA200 для лонга)

Use Volume Filter — объём должен быть ≥ 1.5× среднего за 20 баров

Min Volume Multiplier — нижний порог объёма (рек. 1.5)

Max Volume Multiplier — верхний порог (рек. 3.0–4.0), отсекает аномальные пампы

Use ATR Volatility Filter — минимальная волатильность (рек. 0.3%)

Use Time Filter (UTC) — торговля только в часы высокой ликвидности: 12:00–18:00 и 20:00–02:00 UTC

💡 Идеальна для ручной торговли или подключения сигнальных ботов.

🇬🇧 DESCRIPTION (ENGLISH)

U.T.M.S v2 — Clean EMA Crossover with Filters

Strategy for 15m (primarily) and 1h timeframes.

Generates signals when the EMA(8) and EMA(19) cross, only if trend, volume, volatility, and time of day are confirmed.

Each trade is closed with a fixed Take Profit and Stop Loss.

✅ Low noise, high-quality signals

✅ Active only during high-liquidity hours

✅ Fully protected against flat and fakeouts

🔧 Inputs:

Fast EMA / Slow EMA — moving average periods (default: 8 / 19)

Take Profit % — profit target (suggested: 2.5%)

Stop Loss % — stop loss level (suggested: 2.0%)

Filters (all enabled by default):

Use 1H Trend Filter — trades only in 1H trend direction (EMA50 > EMA200 for long)

Use Volume Filter — volume must be ≥ 1.5× 20-bar average

Min Volume Multiplier — minimum volume threshold (suggested: 1.5)

Max Volume Multiplier — maximum volume cap (suggested: 3.0–4.0), filters out pumps/dumps

Use ATR Volatility Filter — minimum volatility (suggested: 0.3%)

Use Time Filter (UTC) — active only during high-liquidity sessions: 12:00–18:00 & 20:00–02:00 UTC

💡 Perfect for manual trading or webhook-based signal bots.

TurtleTrader Intraday Extended by exp3rts🐢 TurtleTrader Intraday Extended by exp3rts

A modern intraday adaptation of the classic Turtle Trading strategy, optimized for short-term breakout trading with built-in risk management, pyramiding, and optional trend filters.

This strategy captures strong directional moves by entering breakouts from price channels, using ATR-based stop losses and controlled position scaling.

🔑 Key Features:

📈 Channel Breakout Entries: Buy/sell on breakout of highest highs or lowest lows

🛑 Dynamic ATR Stop Loss: Automatically calculated from market volatility

🔁 Pyramiding: Adds up to 4 positions as price moves in your favor

🔄 Directional Mode: Choose Long-only or Short-only mode

🧠 Skip After Win Option: Avoid overtrading by skipping the next entry after a profitable trade

📊 Optional EMA Display: Plot up to 3 EMAs for trend filtering or visual confirmation

📉 On-Chart ATR Label: Displays real-time ATR metrics (including ½N size used in classic Turtle rules)

⚙️ Strategy Inputs:

Entry/Exit channel length

ATR multiplier and period

Entry delay (bar offset)

Optional trade filter after profitable trades

Show/hide EMAs and ATR label

🧪 Best For:

Intraday breakout traders (works well on 5m–1h timeframes)

Traders who prefer mechanical rules and structured risk

Anyone testing volatility-based entries and exits

Inspired by the original Turtle Trading system — redesigned for modern markets with more intraday flexibility and visual enhancements.

RSI Momentum ScalperOverview

The "RSI Momentum Scalper" is a Pine Script v5 strategy crafted for trading highly volatile markets, with a special focus on newly listed cryptocurrencies. This strategy harnesses the Relative Strength Index (RSI) alongside volume analysis and momentum thresholds to pinpoint short-term trading opportunities. It supports both long and short trades, managed with customizable take profit, stop loss, and trailing stop levels, which are visually plotted on the chart for easy tracking.

Why I Created This Strategy

I developed the "RSI Momentum Scalper" because I was seeking a reliable trading strategy tailored to newly listed, highly volatile cryptocurrencies. These assets often experience rapid price fluctuations, rendering traditional strategies less effective. I aimed to create a tool that could exploit momentum and volume spikes while managing risk through adaptable exit parameters. This strategy is designed to address that need, offering a flexible approach for traders in dynamic crypto markets.

How It Works

The strategy utilizes RSI to identify momentum shifts, combined with volume confirmation, to trigger long or short entries. Trades are controlled with take profit, stop loss, and trailing stop levels, which adjust dynamically as the price moves in your favor. The trailing stop helps lock in profits, while the plotted exit levels provide clear visual cues for trade management.

Customizable Settings

The script is highly customizable, allowing you to adjust it to various market conditions and trading styles. Here’s a brief overview of the key settings:

Trade Mode: Select "Both," "Long Only," or "Short Only" to determine the trade direction.

(Default: Both)

RSI Length: Sets the lookback period for the RSI calculation (2 to 30).

(Default: 8)

A shorter length increases RSI sensitivity, suitable for volatile assets.

RSI Overbought: Defines the upper RSI threshold (60 to 99) for short entries.

(Default: 90)

Higher values signal stronger overbought conditions.

RSI Oversold: Defines the lower RSI threshold (1 to 40) for long entries.

(Default: 10)

Lower values indicate stronger oversold conditions.

RSI Momentum Threshold: Sets the minimum RSI momentum change (1 to 15) to trigger entries.

(Default: 14)

Adjusts the sensitivity to price momentum.

Volume Multiplier: Multiplies the volume moving average to filter high-volume bars (1.0 to 3.0).

(Default: 1)

Higher values require stronger volume confirmation.

Volume MA Length: Sets the lookback period for the volume moving average (5 to 50).

(Default: 13)

Influences the volume trend sensitivity.

Take Profit %: Sets the profit target as a percentage of the entry price (0.1 to 10.0).

(Default: 4.15)

Determines when to close a winning trade.

Stop Loss %: Sets the loss limit as a percentage of the entry price (0.1 to 6.0).

(Default: 1.85)

Protects against significant losses.

Trailing Stop %: Sets the trailing stop distance as a percentage (0.1 to 4.0).

(Default: 2.55)

Locks in profits as the price moves favorably.

Visual Features

Exit Levels: Take profit (green), fixed stop loss (red), and trailing stop (orange) levels are plotted when in a position.

Performance Table: Displays win rate, total trades, and net profit in the top-right corner.

How to Use

Add the strategy to your chart in TradingView.

Adjust the input settings based on the cryptocurrency and timeframe you’re trading.

Monitor the plotted exit levels for trade management.

Use the performance table to assess the strategy’s performance over time.

Notes

Test the strategy on a demo account or with historical data before live trading.

The strategy is optimized for short-term scalping; adjust settings for longer timeframes if needed.

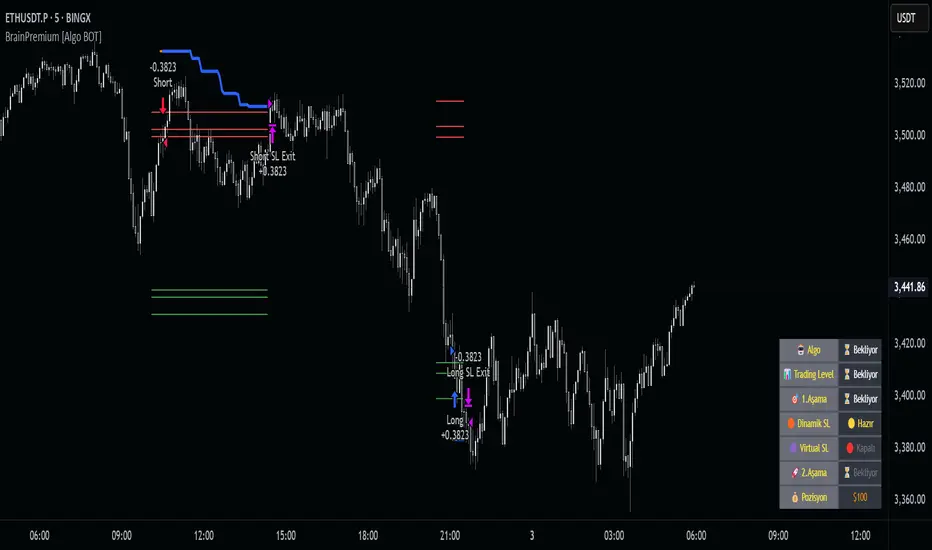

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach:

- **Independent Parameters**: Each trade direction has its own channel settings

- **Asymmetric Trading**: Recognizes that markets often behave differently in uptrends versus downtrends

- **Optimized Performance**: Fine-tune settings for both bullish and bearish conditions

This approach allows the bot to adapt to the natural asymmetry of markets, where uptrends often develop gradually while downtrends can be sharp and sudden.

### Channel Types

#### 1. Keltner Channels

Traditional volatility-based channels using EMA and ATR:

| Setting | Long Default | Short Default |

|---------|--------------|---------------|

| **EMA Length** | 37 | 20 |

| **ATR Length** | 13 | 17 |

| **Multiplier** | 1.4 | 1.9 |

| **Source** | low | high |

- **Strengths**:

- Reliable in trending markets

- Less prone to whipsaws than Bollinger Bands

- Clear visual representation of volatility

- **Weaknesses**:

- Can lag during rapid market changes

- Less effective in choppy, non-trending markets

#### 2. Machine Learning Moving Average (MLMA)

Advanced predictive model using kernel regression (RBF kernel):

| Setting | Description | Options |

|---------|-------------|--------|

| **Source MA** | Price data used for MA calculations | Any price source (low/high/close/etc.) |

| **Moving Average Type** | Type of MA algorithm for calculations | SMA, EMA, WMA, VWMA, RMA, HMA |

| **Trend Source** | Price data used for trend determination | Any price source (close default) |

| **Window Size** | Historical window for MLMA calculations | 5+ (default: 16) |

| **Forecast Length** | Number of bars to forecast ahead | 1+ (default: 3) |

| **Noise Parameter** | Controls smoothness of prediction | 0.01+ (default: ~0.43) |

| **Band Multiplier** | Multiplier for channel width | 0.1+ (default: 0.5-0.6) |

- **Strengths**:

- Predictive rather than reactive

- Adapts quickly to changing market conditions

- Better at identifying trend reversals early

- **Weaknesses**:

- More computationally intensive

- Requires careful parameter tuning

- Can be sensitive to input data quality

### Entry Strategies

| Strategy | Description | Ideal Market Conditions |

|----------|-------------|-------------------------|

| **Breakout** | Enters when price breaks through channel bands, indicating strong momentum | High volatility, emerging trends |

| **Pullback** | Enters when price retraces to the middle band after testing extremes | Established trends with regular pullbacks |

| **Mean Reversion** | Enters at channel extremes, betting on a return to the mean | Range-bound or oscillating markets |

#### Breakout Strategy (Default)

- **Implementation**: Enters long when price crosses above the upper band, short when price crosses below the lower band

- **Strengths**: Captures strong momentum moves, performs well in trending markets

- **Weaknesses**: Can lead to late entries, higher risk of false breakouts

- **Optimization Tips**:

- Increase channel multiplier for fewer but more reliable signals

- Combine with volume confirmation for better accuracy

#### Pullback Strategy

- **Implementation**: Enters long when price pulls back to middle band during uptrend, short during downtrend pullbacks

- **Strengths**: Better entry prices, lower risk, higher probability setups

- **Weaknesses**: Misses some strong moves, requires clear trend identification

- **Optimization Tips**:

- Use with trend filters to confirm overall direction

- Adjust middle band calculation for market volatility

#### Mean Reversion Strategy

- **Implementation**: Enters long at lower band, short at upper band, expecting price to revert to the mean

- **Strengths**: Excellent entry prices, works well in ranging markets

- **Weaknesses**: Dangerous in strong trends, can lead to fighting the trend

- **Optimization Tips**:

- Implement strong trend filters to avoid counter-trend trades

- Use smaller position sizes due to higher risk nature

### Confirmation Indicators

#### Pivot Point SuperTrend

Combines pivot points with ATR-based SuperTrend for trend confirmation:

| Setting | Default Value |

|---------|---------------|

| **Pivot Period** | 25 |

| **ATR Factor** | 2.2 |

| **ATR Period** | 41 |

- **Function**: Identifies significant market turning points and confirms trend direction

- **Implementation**: Requires price to respect the SuperTrend line for trade confirmation

#### Weighted Moving Average (WMA)

Provides additional confirmation layer for entries:

| Setting | Default Value |

|---------|---------------|

| **Period** | 15 |

| **Source** | ohlc4 (average of Open, High, Low, Close) |

- **Function**: Confirms trend direction and filters out low-quality signals

- **Implementation**: Price must be above WMA for longs, below for shorts

### Exit Strategies

#### On-Balance Volume (OBV) Based Exits

Uses volume flow to identify potential reversals:

| Setting | Default Value |

|---------|---------------|

| **Source** | ohlc4 |

| **MA Type** | HMA (Options: SMA, EMA, WMA, RMA, VWMA, HMA) |

| **Period** | 22 |

- **Function**: Identifies divergences between price and volume to exit before reversals

- **Implementation**: Exits when OBV crosses its moving average in the opposite direction

- **Customizable MA Type**: Different MA types provide varying sensitivity to OBV changes:

- **SMA**: Traditional simple average, equal weight to all periods

- **EMA**: More weight to recent data, responds faster to price changes

- **WMA**: Weighted by recency, smoother than EMA

- **RMA**: Similar to EMA but smoother, reduces noise

- **VWMA**: Factors in volume, helpful for OBV confirmation

- **HMA**: Reduces lag while maintaining smoothness (default)

#### ADX Exit Confirmation

Uses Average Directional Index to confirm trend exhaustion:

| Setting | Default Value |

|---------|---------------|

| **ADX Threshold** | 35 |

| **ADX Smoothing** | 60 |

| **DI Length** | 60 |

- **Function**: Confirms trend weakness before exiting positions

- **Implementation**: Requires ADX to drop below threshold or DI lines to cross

## Filter System

### RSI Filter

- **Function**: Controls entries based on momentum conditions

- **Parameters**:

- Period: 15 (default)

- Overbought level: 71

- Oversold level: 23

- Multi-timeframe support: Current, MTF1 (15min), or MTF2 (4h)

- Customizable price source (open, high, low, close, hl2, hlc3, ohlc4)

- **Implementation**: Blocks long entries when RSI > overbought, short entries when RSI < oversold

### Volatility Filter

- **Function**: Prevents trading during excessive market volatility

- **Parameters**:

- Measure: ATR (Average True Range)

- Period: Customizable (default varies by timeframe)

- Threshold: Adjustable multiplier

- Multi-timeframe support

- Customizable price source

- **Implementation**: Blocks trades when current volatility exceeds threshold × average volatility

### Volume Filter

- **Function**: Ensures adequate market liquidity for trades

- **Parameters**:

- Threshold: 0.4× average (default)

- Measurement period: 5 (default)

- Moving average type: Customizable (HMA default)

- Multi-timeframe support

- Customizable price source

- **Implementation**: Requires current volume to exceed threshold × average volume

### Bollinger Bands Filter

- **Function**: Controls entries based on price relative to statistical boundaries

- **Parameters**:

- Period: Customizable

- Standard deviation multiplier: Adjustable

- Moving average type: Customizable

- Multi-timeframe support

- Customizable price source

- **Implementation**: Can require price to be within bands or breaking out of bands depending on strategy

### KEMAD Filter (Kalman EMA Distance)

- **Function**: Advanced trend confirmation using Kalman filter algorithm

- **Parameters**:

- Process Noise: 0.35 (controls smoothness)

- Measurement Noise: 24 (controls reactivity)

- Filter Order: 6 (higher = more smoothing)

- ATR Length: 8 (for bandwidth calculation)

- Upper Multiplier: 2.0 (for long signals)

- Lower Multiplier: 2.7 (for short signals)

- Multi-timeframe support

- Customizable visual indicators

- **Implementation**: Generates signals based on price position relative to Kalman-filtered EMA bands

## Risk Management System

### Position Sizing

Automatically calculates position size based on account equity and risk parameters:

| Setting | Default Value |

|---------|---------------|

| **Risk % of Equity** | 50% |

- **Implementation**:

- Position size = (Account equity × Risk %) ÷ (Entry price × Stop loss distance)

- Adjusts automatically based on volatility and stop placement

- **Best Practices**:

- Start with lower risk percentages (1-2%) until strategy is proven

- Consider reducing risk during high volatility periods

### Stop-Loss Methods

Multiple stop-loss calculation methods with separate configurations for long and short positions:

| Method | Description | Configuration |

|--------|-------------|---------------|

| **ATR-Based** | Dynamic stops based on volatility | ATR Period: 14, Multiplier: 2.0 |

| **Percentage** | Fixed percentage from entry | Long: 1.5%, Short: 1.5% |

| **PIP-Based** | Fixed currency unit distance | 10.0 pips |

- **Implementation Notes**:

- ATR-based stops adapt to changing market volatility

- Percentage stops maintain consistent risk exposure

- PIP-based stops provide precise control in stable markets

### Trailing Stops

Locks in profits by adjusting stop-loss levels as price moves favorably:

| Setting | Default Value |

|---------|---------------|

| **Stop-Loss %** | 1.5% |

| **Activation Threshold** | 2.1% |

| **Trailing Distance** | 1.4% |

- **Implementation**:

- Initial stop remains fixed until profit reaches activation threshold

- Once activated, stop follows price at specified distance

- Locks in profit while allowing room for normal price fluctuations

### Risk-Reward Parameters

Defines the relationship between risk and potential reward:

| Setting | Default Value |

|---------|---------------|

| **Risk-Reward Ratio** | 1.4 |

| **Take Profit %** | 2.4% |

| **Stop-Loss %** | 1.5% |

- **Implementation**:

- Take profit distance = Stop loss distance × Risk-reward ratio

- Higher ratios require fewer winning trades for profitability

- Lower ratios increase win rate but reduce average profit

### Filter Combinations

The strategy allows for simultaneous application of multiple filters:

- **Recommended Combinations**:

- Trending markets: RSI + KEMAD filters

- Ranging markets: Bollinger Bands + Volatility filters

- All markets: Volume filter as minimum requirement

- **Performance Impact**:

- Each additional filter reduces the number of trades

- Quality of remaining trades typically improves

- Optimal combination depends on market conditions and timeframe

### Multi-Timeframe Filter Applications

| Filter Type | Current Timeframe | MTF1 (15min) | MTF2 (4h) |

|-------------|-------------------|-------------|------------|

| RSI | Quick entries/exits | Intraday trend | Overall trend |

| Volume | Immediate liquidity | Sustained support | Market participation |

| Volatility | Entry timing | Short-term risk | Regime changes |

| KEMAD | Precise signals | Trend confirmation | Major reversals |

## Visual Indicators and Chart Analysis

The bot provides comprehensive visual feedback on the chart:

- **Channel Bands**: Keltner or MLMA bands showing potential support/resistance

- **Pivot SuperTrend**: Colored line showing trend direction and potential reversal points

- **Entry/Exit Markers**: Annotations showing actual trade entries and exits

- **Risk/Reward Zones**: Visual representation of stop-loss and take-profit levels

These visual elements allow for:

- Real-time strategy assessment

- Post-trade analysis and optimization

- Educational understanding of the strategy logic

## Implementation Guide

### TradingView Setup

1. Load the script in TradingView Pine Editor

2. Apply to your preferred chart and timeframe

3. Adjust parameters based on your trading preferences

4. Enable alerts for webhook integration

### Webhook Integration

1. Configure webhook URL in TradingView alerts

2. Set up receiving endpoint on your trading platform

3. Define message format matching the bot's output

4. Test with small position sizes before full deployment

### Optimization Process

1. Backtest across different market conditions

2. Identify parameter sensitivity through multiple tests

3. Focus on risk management parameters first

4. Fine-tune entry/exit conditions based on performance metrics

5. Validate with out-of-sample testing

## Performance Considerations

### Strengths

- Adaptability to different market conditions through dual channels

- Multiple layers of confirmation reducing false signals

- Comprehensive risk management protecting capital

- Machine learning integration for predictive edge

### Limitations

- Complex parameter set requiring careful optimization

- Potential over-optimization risk with so many variables

- Computational intensity of MLMA calculations

- Dependency on proper webhook configuration for execution

### Best Practices

- Start with conservative risk settings (1-2% of equity)

- Test thoroughly in demo environment before live trading

- Monitor performance regularly and adjust parameters

- Consider market regime changes when evaluating results

## Conclusion

The ₿ober XM v2.0 represents a significant evolution in trading strategy design, combining traditional technical analysis with machine learning elements and multi-timeframe analysis. The core strength of this system lies in its adaptability and recognition of market asymmetry.

### Market Asymmetry and Adaptive Approach

The strategy acknowledges a fundamental truth about markets: bullish and bearish phases behave differently and should be treated as distinct environments. The dual-channel system with separate parameters for long and short positions directly addresses this asymmetry, allowing for optimized performance regardless of market direction.

### Targeted Backtesting Philosophy

It's counterproductive to run backtests over excessively long periods. Markets evolve continuously, and strategies that worked in previous market regimes may be ineffective in current conditions. Instead:

- Test specific market phases separately (bull markets, bear markets, range-bound periods)

- Regularly re-optimize parameters as market conditions change

- Focus on recent performance with higher weight than historical results

- Test across multiple timeframes to ensure robustness

### Multi-Timeframe Analysis as a Game-Changer

The integration of multi-timeframe analysis fundamentally transforms the strategy's effectiveness:

- **Increased Safety**: Higher timeframe confirmations reduce false signals and improve trade quality

- **Context Awareness**: Decisions made with awareness of larger trends reduce adverse entries

- **Adaptable Precision**: Apply strict filters on lower timeframes while maintaining awareness of broader conditions

- **Reduced Noise**: Higher timeframe data naturally filters market noise that can trigger poor entries

The ₿ober XM v2.0 provides traders with a framework that acknowledges market complexity while offering practical tools to navigate it. With proper setup, realistic expectations, and attention to changing market conditions, it delivers a sophisticated approach to systematic trading that can be continuously refined and optimized.

Follow Line Strategy Version 2.5 (React HTF)Follow Line Strategy v2.5 (React HTF) - TradingView Script Usage

This strategy utilizes a "Follow Line" concept based on Bollinger Bands and ATR to identify potential trading opportunities. It includes advanced features like optional working hours filtering, higher timeframe (HTF) trend confirmation, and improved trend-following entry/exit logic. Version 2.5 introduces reactivity to HTF trend changes for more adaptive trading.

Key Features:

Follow Line: The core of the strategy. It dynamically adjusts based on price breakouts beyond Bollinger Bands, using either the low/high or ATR-adjusted levels.

Bollinger Bands: Uses a standard Bollinger Bands setup to identify overbought/oversold conditions.

ATR Filter: Optionally uses the Average True Range (ATR) to adjust the Follow Line offset, providing a more dynamic and volatility-adjusted entry point.

Optional Trading Session Filter: Allows you to restrict trading to specific hours of the day.

Higher Timeframe (HTF) Confirmation: A significant feature that allows you to confirm trade signals with the trend on a higher timeframe. This can help to filter out false signals and improve the overall win rate.

HTF Selection Method: Choose between Auto and Manual HTF selection:

Auto: The script automatically determines the appropriate HTF based on the current chart timeframe (e.g., 1min -> 15min, 5min -> 4h, 1h -> 1D, Daily -> Monthly).

Manual: Allows you to select a specific HTF using the Manual Higher Timeframe input.

Trend-Following Entries/Exits: The strategy aims to enter trades in the direction of the established trend, using the Follow Line to define the trend.

Reactive HTF Trend Changes: v2.5 exits positions not only based on the trade timeframe (TTF) trend changing, but also when the higher timeframe trend reverses against the position. This makes the strategy more responsive to larger market movements.

Alerts: Provides buy and sell alerts for convenient trading signal notifications.

Visualizations: Plots the Follow Line for both the trade timeframe and the higher timeframe (optional), making it easy to understand the strategy's logic.

How to Use:

Add to Chart: Add the "Follow Line Strategy Version 2.5 (React HTF)" script to your TradingView chart.

Configure Settings: Customize the strategy's settings to match your trading style and preferences. Here's a breakdown of the key settings:

Indicator Settings:

ATR Period: The period used to calculate the ATR. A smaller period is more sensitive to recent price changes.

Bollinger Bands Period: The period used for the Bollinger Bands calculation. A longer period results in smoother bands.

Bollinger Bands Deviation: The number of standard deviations from the moving average that the Bollinger Bands are plotted. Higher deviations create wider bands.

Use ATR for Follow Line Offset?: Enable to use ATR to calculate the Follow Line offset. Disable to use the simple high/low.

Show Trade Signals on Chart?: Enable to show BUY/SELL labels on the chart.

Time Filter:

Use Trading Session Filter?: Enable to restrict trading to specific hours of the day.

Trading Session: The trading session to use (e.g., 0930-1600 for regular US stock market hours). Use 0000-2400 for all hours.

Higher Timeframe Confirmation:

Enable HTF Confirmation?: Enable to use the HTF trend to filter trade signals. If enabled, only trades in the direction of the HTF trend will be taken.

HTF Selection Method: Choose between "Auto" and "Manual" HTF selection.

Manual Higher Timeframe: If "Manual" is selected, choose the specific HTF (e.g., 240 for 4 hours, D for daily).

Show HTF Follow Line?: Enable to plot the HTF Follow Line on the chart.

Understanding the Signals:

Buy Signal: The price breaks above the upper Bollinger Band, and the HTF (if enabled) confirms the uptrend.

Sell Signal: The price breaks below the lower Bollinger Band, and the HTF (if enabled) confirms the downtrend.

Exit Long: The trade timeframe trend changes to downtrend or the higher timeframe trend changes to downtrend.

Exit Short: The trade timeframe trend changes to uptrend or the higher timeframe trend changes to uptrend.

Alerts:

The script includes alert conditions for buy and sell signals. To set up alerts, click the "Alerts" button in TradingView and select the desired alert condition from the script. The alert message provides the ticker and interval.

Backtesting and Optimization:

Use TradingView's Strategy Tester to backtest the strategy on different assets and timeframes.

Experiment with different settings to optimize the strategy for your specific trading style and risk tolerance. Pay close attention to the ATR Period, Bollinger Bands settings, and the HTF confirmation options.

Tips and Considerations:

HTF Confirmation: The HTF confirmation can significantly improve the strategy's performance by filtering out false signals. However, it can also reduce the number of trades.

Risk Management: Always use proper risk management techniques, such as stop-loss orders and position sizing, when trading any strategy.

Market Conditions: The strategy may perform differently in different market conditions. It's important to backtest and optimize the strategy for the specific markets you are trading.

Customization: Feel free to modify the script to suit your specific needs. For example, you could add additional filters or entry/exit conditions.

Pyramiding: The pyramiding = 0 setting prevents multiple entries in the same direction, ensuring the strategy doesn't compound losses. You can adjust this value if you prefer to pyramid into winning positions, but be cautious.

Lookahead: The lookahead = barmerge.lookahead_off setting ensures that the HTF data is calculated based on the current bar's closed data, preventing potential future peeking bias.

Trend Determination: The logic for determining the HTF trend and reacting to changes is critical. Carefully review the f_calculateHTFData function and the conditions for exiting positions to ensure you understand how the strategy responds to different market scenarios.

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice, and you should not trade based solely on the signals generated by this script. Always do your own research and consult with a qualified financial advisor before making any trading decisions. The author is not responsible for any losses incurred as a result of using this script.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

FVG Breakout Lite by tradingbauhausExplanation of "FVG Breakout Lite by tradingbauhaus"

This script is a trading strategy built for TradingView that helps you spot and trade "Fair Value Gaps" (FVGs)—price areas where the market moved quickly, leaving a gap that might act as support or resistance later. It’s designed to catch breakout opportunities when the price moves strongly in one direction, with extra filters to make trades more reliable. Here’s how it works and how you can use it:

What It Does

1. Finds Fair Value Gaps (FVGs):

A "Bullish FVG" happens when the price jumps up quickly, leaving a gap below where it didn’t trade much (e.g., today’s low is higher than the high from two bars ago).

A "Bearish FVG" is the opposite: the price drops fast, leaving a gap above (e.g., today’s high is lower than the low from two bars ago).

The script draws colored boxes on your chart to show these gaps: green for bullish, red for bearish.

2. Spots Breakouts:

It looks for "strong" FVGs by comparing them to a trend (based on the highest highs and lowest lows over a set period).

If a bullish gap forms above the recent highs, or a bearish gap below the recent lows, it’s marked as a breakout opportunity.

3. Adds a Volume Check:

Trades only happen if the market’s volume is higher than usual (e.g., 1.2x the average volume over the last 20 bars). This helps ensure the breakout has real momentum behind it.

4. Trades Automatically:

Long Trades (Buy): If a bullish breakout FVG forms and volume is high, it buys at the current price.

Short Trades (Sell): If a bearish breakout FVG forms with high volume, it sells short.

Each trade comes with a stop loss (to limit losses) and a take profit (to lock in gains), both adjustable by you.

5. Shows Mitigation Lines (Optional):

If you turn on "Display Mitigation Zones," it draws lines at the edge of each breakout FVG. These lines show where the price might return to "fill" the gap later, helping you see key levels.

6. Includes Webull Costs:

The script factors in real trading fees from Webull, like tiny SEC and FINRA fees for selling, and a daily margin cost if you’re borrowing money to trade. These don’t show up on the chart but affect the strategy’s performance in backtesting.

How to Use It

1. Add to Your Chart:

Copy the script into TradingView’s Pine Editor, click "Add to Chart," and it’ll start drawing FVGs and running the strategy.

2. Customize Settings:

Trend Period (Default: 25): How many bars it looks back to define the trend. Longer periods mean fewer but stronger signals.

Volume Lookback (Default: 20) & Volume Threshold (Default: 1.2): Adjust how it measures "high volume." Increase the threshold for stricter trades.

Stop Loss % (Default: 1.5%) & Take Profit % (Default: 3%): Set how much you’re willing to lose or aim to gain per trade.

Margin Rate % (Default: 8.74%): Webull’s rate for borrowing money—lower it if your account qualifies for a better rate.

Display Mitigation Zones (Default: On): Toggle this to see or hide the gap lines.

Colors: Change the green (bullish) and red (bearish) shades to suit your chart.

3. Backtest It:

Go to the "Strategy Tester" tab in TradingView to see how it performs on past data. It’ll show trades, profits, losses, and Webull fees included.

4. Watch It Work:

Green boxes mean bullish FVGs; red boxes mean bearish FVGs. If volume spikes and the price breaks out, you’ll see trades happen automatically.

What to Expect

Visuals: You’ll see colored boxes for FVGs and optional lines showing where they start. These help you spot key price zones even if you’re not trading.

Trades: It’s selective—only trades when FVGs align with a breakout and volume confirms it. Expect fewer trades but with higher potential.

Risk: The stop loss keeps losses in check, while the take profit aims for a 2:1 reward-to-risk ratio by default (3% gain vs. 1.5% loss).

Costs: Webull’s fees are small but baked into the results, so you’re seeing a realistic picture of profits.

Tips for Users

Test it on a small timeframe (like 5-minute charts) for day trading or a larger one (like daily) for swing trading.

Play with the volume threshold—if you get too few trades, lower it (e.g., 1.1); if too many, raise it (e.g., 1.5).

Watch how price reacts to the mitigation lines—they’re often support or resistance zones traders target.

This strategy is lightweight, focused, and built for traders who like breakouts with a bit of confirmation. It’s not foolproof (no strategy is!), but it gives you a clear way to trade FVGs with some smart filters.

IronBot v4IronBot v4 – Trading Strategy Overview

1. Quick Context

IronBot v4 is a trading strategy designed for users who want a simple yet effective approach to reading the markets. It uses a combination of Fibonacci retracement levels, custom logic triggers, and innovative modules (EMA validation, Iron Impulse Shield and Iron Auto Volume Detector) to identify potential entry and exit points, strengthening the strategy’s detection of sudden market volatility or shifts in trading volume.

2. Theoretical Details

Fibonacci Analysis

The script identifies recent market highs and lows, then calculates key Fibonacci levels (high- and low-based). These levels can help confirm potential reversals or trends.

EMA Option

When enabled, the exponential moving average (EMA) offers additional validation for trade entries. If the current price remains above a certain EMA threshold, long positions may be favored; conversely, if it stays below the EMA, short positions may be initiated.

IIS (Iron Impulse Shield)

IIS helps to filter out risky trades by measuring recent price shocks or surges. If an extreme movement is detected, the strategy may temporarily disable longs or shorts to avoid false signals.

IAVD (Iron Auto Volume Detector)

This functionality automatically detects the average market volume over a defined period (regardless of the market, since it relies on real data). When entering a position, it ensures that overall volume is high enough to confirm a genuinely active, robust market. By providing an additional filter, it can strengthen the decision-making process whenever the market’s participation level is in question.

Panel

IronBot v4 displays a real-time backtest panel that summarizes the selected configuration (including the current pair, analysis window, enabled filters), as well as showing net profit, applicable exchange fees, country taxes, and the final net balance. This gives traders an immediate overview of strategy performance and risk metrics.

What Pinescript Adds Visually

The script plots:

Fibonacci levels (highlighting potential reversal zones)

Trend lines indicating bullish (green) or bearish (red) lean

Optional EMA line

Optional Fibonacci forecast lines for anticipating future moves

Automatic labeling of entry, take-profit, and stop-loss levels, indicating the profit percentage of each trade.

3. Explanation of Inputs

The strategy exposes multiple inputs that can be toggled or configured by the user:

Analysis Window : Dictates how many bars to consider for high/low calculations and the fib retracement thresholds.

TRADES

Display TP/SL: For displaying Take profits and Stop loss.

Display Forecast: When enabled, this feature calculates and projects possible future Fibonacci retracements using historical data, helping traders anticipate potential upcoming trade setups.

Leverage: Only used for the Panel and not for trades. Lets you amplify your position size; higher leverage increases potential gains but also heightens risk. TradingView strategy is using properties for doing this.

Exchange Maker Fees & Exchange Taker Fees: Only used for the Panel and not for trades. Define the percentage cost applied by your exchange for maker and taker trades, respectively. These fees are accounted for in final profit calculations of the Panel.

Country Tax: Only used for the Panel and not for trades. Specifies a tax percentage to be deducted from net profits.

STOP LOSS and TAKE PROFITS

Stop-Loss & Take-Profit Parameters: Controls the percentage distances at which the strategy will exit positions. Additionally, you can configure up to four distinct take-profit levels (TP1 through TP4). Each level should be higher target than the previous one, and you can assign a specific percentage of the total position to close at each TP, ensuring the sum equals 100%. A break-even feature is also available when multiple TPs are used.

EMA

EMA (Exponential Moving Average) Option: When enabled, the strategy opens long trades only if the current price is above the specified EMA length, and opens short trades only if it is below that threshold.

PANELS

Show Panel: For displaying the backtest integrated panel.

IRON IMPULSE SHIELD (IIS)

IIS (Iron Impulse Shield) Option: When enabled, IIS continuously monitors recent price volatility depending on the analysis window set. If the market experiences an extreme surge or drop beyond a specified threshold, IIS temporarily blocks new long or short positions.

IRON AUTO VOLUME DETECTOR (IAVD)

IAVD (Iron Auto Volume Detector) Option: When enabled, it continuously measures the average market volume over a special period, irrespective of the specific trading pair. This ensures that IronBot v4 focuses on markets with robust participation, reducing the likelihood of entering trades during low-liquidity conditions.

By changing these values, IronBot v4 reacts differently to market structure and risk management requirements. Stop-loss and take-profit levels will adjust accordingly, while advanced filters (like EMA or IIS) influence when trades can open.

4. TradingView Strategy Properties

IronBot v4 uses the built-in TradingView “strategy” functionality. In particular:

Order Placement: The code calls strategy.entry() and strategy.close() for direct orders, ensuring signals are sent immediately (no limit orders are used). This helps connect with exchange signal bots for automated execution.

Initial Capital: The code uses initial capital defined in properties for calculating Net balance in the integrated panel.

On bar close: This strategy fill orders on bar close.

Pyramiding: This strategy can take only 1 successive trade in the same direction

Be careful to configure your leverage input depending on your strategy properties.

5. Visualization

5. Purpose & Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always confirm your own risk tolerance and consult a financial professional before placing live trades. Trading leveraged products can involve substantial risk of loss.

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)